People love to debate whether it makes more sense to rent or buy. So instead of vague hypotheticals, let’s use two actual homes sitting half a mile apart in Beaverton right now.

- For Rent: 16827 SW Shelby Ct — $2,995/mo on Zillow.

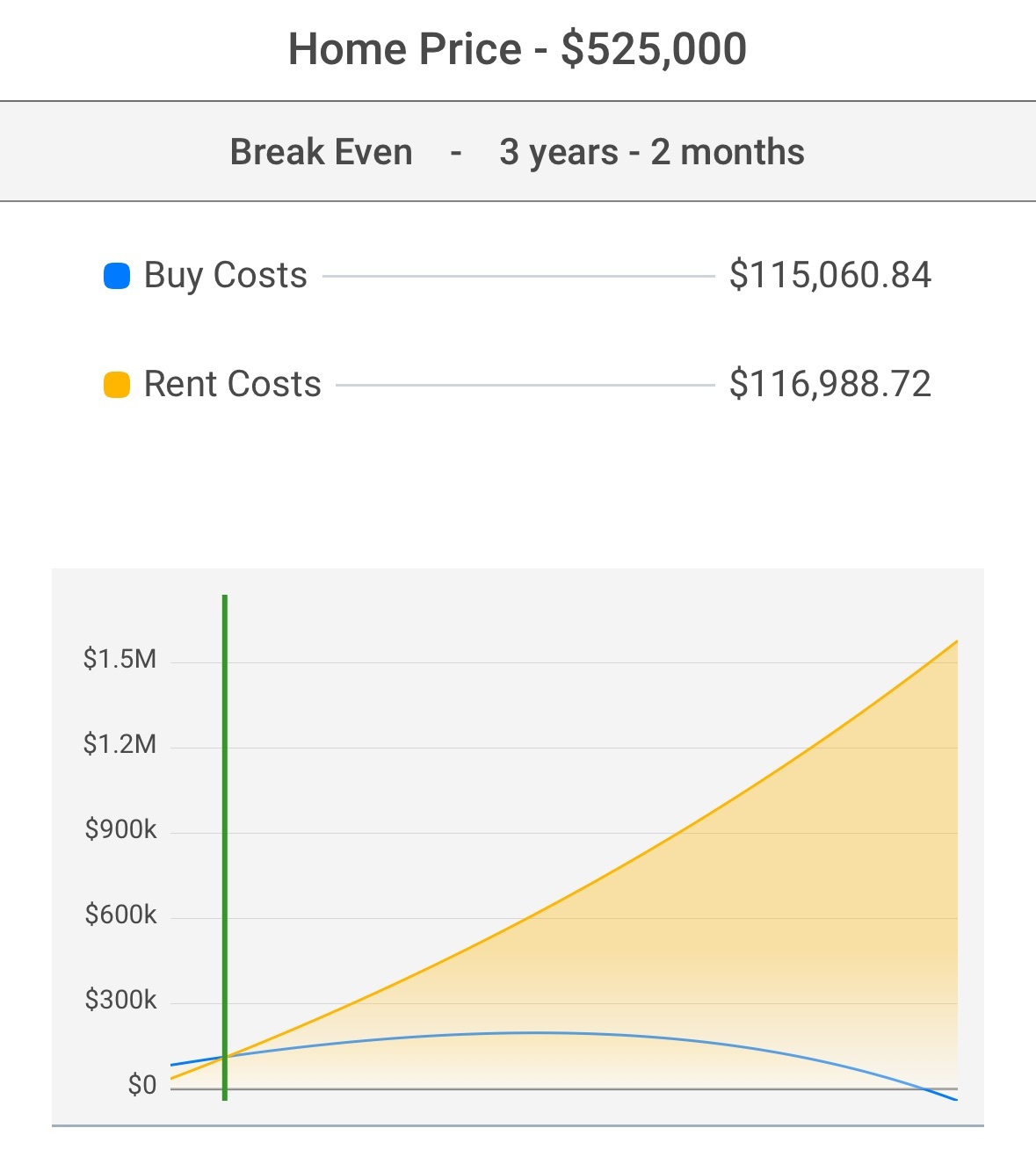

- Just Sold: 16838 SW Cynthia St — closed at $525,000 (listed for $540,000).

Same neighborhood. Same vibe. But the difference between paying rent and owning? That’s where things get real.

What Buying Looks Like

Let’s say you scooped up Cynthia St. with 10% down.

- Purchase price: $525,000

- Down payment: $52,500

- Loan amount: $472,500

- Rate: ~6.375% (as of today)

- Estimated mortgage payment with taxes, insurance, PMI, etc: $3,619/mo

But here’s the thing: as a homeowner, you can deduct the interest you’re paying on your loan. That tax benefit shakes out to around $549/month back in your pocket. Which brings your “tax-adjusted” mortgage payment down to $3,070/mo.

That’s about $70 more than the rent on Shelby Ct. For 70 bucks, you’re buying a home — not renting one.

The Long Game: Rent vs. Equity

Here’s where it gets fun. Let’s compare renting vs. buying over a little more than three years:

- Rent: Assuming a modest 2.5% annual increase (super conservative for Portland), your payment goes up to about $3,233/mo. And after 38 months, you’ve built exactly $0 in equity. Congrats, your landlord loves you.

- Buying: With 3.5% annual appreciation, plus your down payment and the principal you’ve chipped away at, you’re sitting on around $131,298 in equity.

Three years and two months. That’s your breakeven point where owning actually costs less than renting. And from there, the gap only gets wider.

So Why Rent?

Look, I’m not here to dump on renters. I’ve rented plenty myself. Sometimes it’s the right move for flexibility or because you’re not ready yet. But here’s the reality: a lot of people can qualify for a mortgage and just don’t know it. Or they’re waiting for “perfect” rates.

Meanwhile, equity is slipping through your fingers. Every rent check you write is just paying down somebody else’s mortgage. Every month you wait is another month you don’t own a damn thing.

So ask yourself: in three years, do you want to look back and have a home with over $130K in equity… or do you want to look back and realize you spent the same money and have absolutely nothing to show for it?

👉 Ready to talk through your options? Let’s run your numbers and see if buying makes sense for you right now. Worst case, we grab a coffee and I’ll tell you if renting is still your best move. Best case? You stop paying your landlord’s mortgage and start paying your own.